For my sins I seem to have spent a fair bit of time in the company of sales people from the big ERP vendors in the last few weeks. One of the last bastions of on-premise thinking, enterprise resource planning (AKA “the finance system”) is starting to see its transition into the world of Software as a Service.

For some years now it’s been clear to me that moving from a software licensing to SaaS model is much more than a mere switch in infrastructure. Becoming a cloud provider means a significant shift in business model for both supplier and customer. The traditional vendors have struggled.

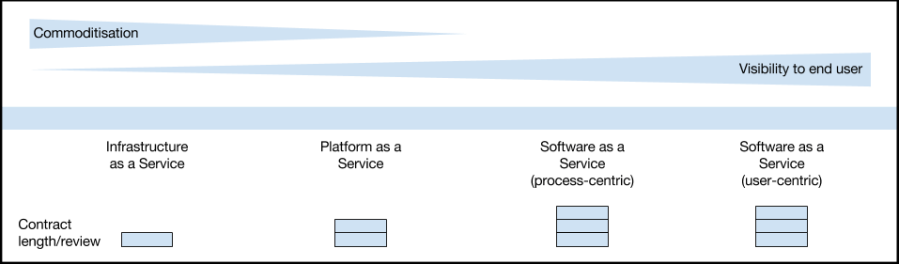

What’s becoming more apparent to me is that there is also significant difference in the business models associated with different types of cloud product.

Over in the left hand side, pure Infrastructure as a Service (compute, storage, low level services like DNS) are commodities. They are like bags of sugar (ish) – fungible stuff that can be swapped in and out without impact to the users consuming the services that have been built above. AWS one day, Azure the next. Price is likely to be the differentiator. You buy commodities in a marketplace. Brand might have some influence, but you’re basically then buying Heinz over own-brand.

Platform as a Service is more of a product. Not all AI is created equal. I guess here you are buying on functionality until those functions become commoditized and end up as value-add in IaaS? New PaaS products will fill their place. None of this stuff is directly visible to end users – but the functionality provided will (should) be important. PaaS is a sell to technologists. Inevitably there will be a lot of shiny shiny.

Process-centric Software as a Service might be sold into the IT department, or to the management of the target part of the organisations (the Salesforce “No Software” model of selling direct to heads of sales teams). CRM and ERP (the two biggest categories of process-centric SaaS) embed deeply into an organisation, and you would expect to be

End user-centric Software as a Service is an interesting one. For vendors there are two routes to market. You either target the enterprise IT buyer, purchasing on behalf of their users, or you go for the end users themselves. Both strategies can be effective, although I’d argue the former more so if you are selling something new over a cloud variant of an existing product category. Slack has captured hearts and minds by selling directly to small product teams whereas Office 365 appears to have won the battle of the productivity suite.

These tools, whilst not hard-wired into business process, are anything but commodity because of the upheaval involved in moving users from one platform to another. Sure email is email, but GMail is not Outlook, Docs not Word etc etc.

(As an aside, it’s been occurring to me that Google G-Suite using organisations might by definition be more likely to be the sorts of organisations that use more modern tools like Slack or Trello. Therefore I wonder if G-Suite is more prone to disruption from those substitution products, shortening the lifetime there of the old skool Office suite?)

To change stuff on the right hand side you need to change the way in which people behave. That takes time, effort and cost. Often the depth of that cost (down to individual productivity) is significantly overlooked (paradoxically whilst the benefits of the same are significantly overplayed in business cases). The stuff on the right-hand side will be powered by commoditised stuff on the left, but that doesn’t mean that they are commodities.

As a result, whilst pure utility computing power at the far left can in principle and practice be swapped in and out from providers (and therefore be purchased through marketplaces), the longer term commitment on the right would necessitate acquisition models that ensure the analysis of business and user needs, and also time to assess the impact of a new commitment. You should expect to commit to stuff on the right hand side for far longer than the stuff on the left.

One other thing that has struck me from doing this analysis is that most vendors focus much of their activity in only one or two of these segments. The notable exception is Microsoft, who have products spanning every category. That has the potential for a challenging client/supplier relationship as the different categories of product will necessitate quite different sales and service approaches with much more variation than existed when the thing being sold was a software licence.